A growing force in the automotive industry can’t be ignored.

by Erin Kerrigan

August 14, 2025

Today 64% of vehicles sold in China – a market now double the size of the U.S. – are manufactured and sold by domestic Chinese brands, up from 36% in 2020.

Credit:

Pexels/Aditya Agarwal

3 min to read

China is rapidly redefining the global automotive industry, and potentially the U.S. market.

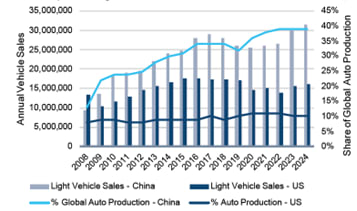

It’s the largest auto retail market in the world, surpassing the U.S. in 2009 (see chart). Now Chinese OEMs are on the verge of becoming the world’s largest automakers. Today China represents 40% of global auto production relative to the 10% U.S. share. The country leverages its superior cost efficiencies, government-backed initiatives and aggressive expansion strategies to accelerate its global market share gains.

Ad Loading...

Sources: China Association of Automobile Manufacturers, CEIC, Macrobond, Automotive News, Kerrigan Advisors’ Research & Analysis

Credit:

Kerrigan Advisors

Today 64% of vehicles sold in China – a market now double the size of the U.S. – are manufactured and sold by domestic Chinese brands, up from 36% in 2020. By contrast, legacy automakers have seen their market share decline to just 36%. The rapid ascent of China’s domestic brands in China, at the expense of imports, signals a potential reshuffling of the global auto industry, with Chinese manufacturers poised to extend their market dominance beyond their home market.

The financial ramifications to legacy OEMs of lost market share in the world’s largest auto market are becoming increasingly apparent. Seventy percent of OEM executives surveyed by Kerrigan Advisors now have concerns about the financial impact of Chinese OEMs’ rising global market share. This is perhaps not surprising when considering how the automakers that suffered the most significant declines in Chinese market share had historically relied on China for a meaningful percentage of their global sales.

OEMs’ concern about the financial impact of their Chinese counterparts are becoming a reality as their earnings are now being negatively impacted by the lost sales. One of the most striking examples is General Motors, which recorded a $5 billion restructuring charge in the fourth quarter of 2024 due to the deterioration of its Chinese business. To put this into perspective, GM’s China charge represents 70% of the company’s 2024 net income, underscoring the financial gravity of the shifting competitive realities.

As legacy OEMs experience the financial fallout from their shrinking China presence, they have concerns about Chinese OEMs entering the lucrative U.S. market, the only major auto retail market in the world where Chinese OEMs are absent. This makes the U.S. a highly attractive auto retail market for legacy OEMs. However, 76% of U.S. auto executives surveyed by Kerrigan Advisors expect Chinese automakers to eventually enter the U.S. market, indicating the barrier to entry may be short-lived.

While the U.S. has successfully shielded its auto retail market from Chinese imports for now, the global rise of Chinese OEMs – and the potential for their future entry into the U.S. – will inevitably impact legacy automakers’ U.S. strategy, operations and associated blue-sky values. Blue sky represents the intangible value of a franchise, driven by an OEM’s ability to sustain a profitable dealer network with compelling, innovative products. When an automaker loses global market share and suffers the financial implications of that loss, its blue-sky value often declines.

Ad Loading...

Whether Chinese vehicles enter the U.S. market directly or not, their growing dominance in the global auto industry will have financial consequences for U.S. auto retailers. As the competitive conditions continue to shift, U.S. dealers should closely monitor the financial health and strategic global positioning of their franchise OEMs, ensuring they align with brands capable of sustained investment and long-term viability in an evolving global marketplace. Fully insulating the U.S. auto market and blue-sky values from the impact of the Chinese auto industry likely has an expiration date.

Erin Kerrigan is founder and managing director of Kerrigan Advisors, a sell-side adviser to U.S. dealerships that has represented on the sale of more than 400 franchises.

EDITOR’S NOTE: This article was authored and edited according to F&I and Showroom editorial standards and style. Opinions expressed may not reflect that of the publication.

Deal volume ebbed and flowed throughout 2025, but product performance remained steady, according to automotive technology and data intelligence solutions provider StoneEagle.

Americans’ view of present business conditions, the labor market and family finances, though, are still in the dumps, and if they plan to buy cars, many target used units.

Auto loan originations rose over 6% year-over-year in the third quarter of 2025, but TransUnion predicts a slight decline in auto loan growth this year, making it an outlier in the company's overall lending forecast.

Edmunds’ editorial team tested 300-plus vehicles to help determine the Top Rated Awards for 2026, and one brand stood out with multiple rankings, including Best of the Best.

February forecast has new-vehicle deliveries still off from last year at this time amid high prices and vanished EV incentives. But J.D. Power sees business picking up from here as automakers target growth.

Study finds that adopters are true believers and that their satisfaction with the vehicles is growing, including for public charger experience, despite pullback of federal incentives.

The sector generates over $64 billion in annual economic impact in South Carolina, making it the largest and fastest-growing manufacturing subsector in the state.